Gold’s swoon has triggered a good deal of schadenfreude, some subtle, some less so.

It’s hardly a surprise after eleven years of gains and often tiresome crowing from its more partisan supporters. Question is, apart from the emotional satisfaction of putting the boot in, are these critics justified?

Their complaints seem to revolve around four principal themes:

• Gold isn’t an investment. It produces no income and should therefore, at best, be regarded as a trade.

• It can’t be valued properly. With no income, and no shortage of existing stocks, the bull case is entirely reliant on an unending supply of greater fools.

• Gold’s supporters are true believers, more akin to members of a cult than rational economic actors.

• In any case, it’s way too volatile to ever be a proper currency, even if that were theoretically possible or desirable. All the fools who bought the “gold is money” pitch are going to get buried.

Well, maybe.

♦ ♦ ♦

In any case, let’s consider them one by one.

• No argument: gold isn’t an investment. If it’s anything (monetarily speaking), it’s base money, or currency. To believe otherwise is a category error. Most serious gold bulls understand that even if the word “investment” is sometimes bandied about carelessly.

Whether “trade” is the right descriptive term is a bit trickier. For some, it certainly is. For others, however, those who categorise gold as money, it’s a precautionary holding, likely to do tolerably well if most other things financial are going down the tubes.

• Can gold be valued properly? Seems more like a zen koan than a question with a clear answer, doesn’t it? At one level, the critics are undoubtedly right: with no income stream and superabundant existing stocks, gold is entirely at the mercy of perceptions. Still, it’s also true that greater fools have shown up with reassuring regularity for the last few thousand years. Is that likely to change any time soon? We’re probably each obliged to answer that question individually. And to accept the consequences.

By the way, while gold doesn’t yield anything, nor does physical currency. To earn anything on either, you have to lend them out.

• It’s certainly true that there’s a sizeable subspecies of goldbugs who are cultlike in the intensity of their beliefs. They have their demons, their gods, their sacred texts, and see this crisis as the final scene in a battle between good and evil. Gold for them is a symbolic lightning rod, not to be subjected to dispassionate analysis, much less ridicule.

Thing is, stripped of this emotional baggage (which is in any case rooted in politics and often religion), their monetary beliefs aren’t without foundation.

There is, after all, a long history of gold as money. Not as the reflection of some quasi-religious belief, but as a matter of cool, pragmatic, bottom-up agreement. It’s what the markets chose and for all its intermittent problems, the (real) gold standard worked well for a long time. Even today central banks all have gold on their radar screens (unaccountably or otherwise) and quite a few are busy acquiring more. Indeed, much of the non-Western world continues to view gold as real money. Foolish? Perhaps, although I don’t think so. In any case, ignoring that possibly uncomfortable fact is even more foolish. After all, right now these are the guys and gals with the savings.

• And yes, it does fluctuate, sometimes a lot. It’s hardly alone though, is it? US stocks fell 23% in one day in 1987 and some 30% in a few weeks in 2008; the yen tumbled 18% in under a week in 1998. And so on.

Did this lead to their dismissal as an asset class? Of course not. These things sometimes happen in markets where speculation has run rife. When the stars then align and players from every time frame suddenly find themselves on the same side of the market, weird stuff happens. Sensible people understand that and form their views accordingly. Certainly, drawing far reaching conclusions from such structural aberrations is plain foolishness.

Time alone will provide the answers to most of these vexing issues. We’d probably be wisest to pay no more attention to the (often amusing) fulminations of the more extreme critics than to those of their targets.

♦ ♦ ♦

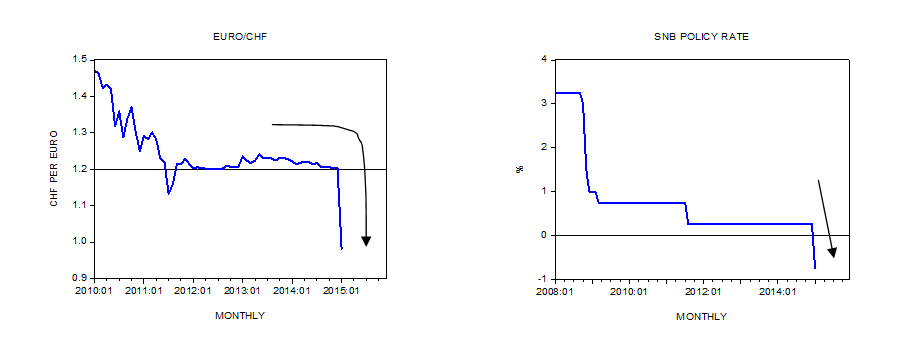

So, has gold bottomed?

Well, nobody knows of course. Short-term, it depends on whether the weak hands are finally out. FWIW, I think most of them probably are. Longer term, what matters are the policies governments and central banks run in years to come. If fiscal and monetary prudence took centre stage, gold would almost certainly go into a long-term nominal bear market. If, as seems to me more likely, the current activist extravagance persists, or intensifies, then the nominal (and probably real) upside still beckons, perhaps with even greater volatility. And, quite possibly, for years to come. We may as yet have only seen Act I.

In any case, caveat emptor.

s

P.S. The title comes courtesy the traditions of a popular Urdu newspaper. According to a friend who once read it regularly, whenever a local notable died it invariably printed a minor editorial with the heading (for example): “Ah! Qasim Rizavi.”

Super summary!

“Gold and silver are money. Everything else is credit”

— J.P. Morgan

Woodrow Wilson on the Federal Reserve System

“I am a most unhappy man. I have unwittingly ruined my country. A great industrial nation is controlled by its system of credit. Our system of credit is concentrated. The growth of the nation, therefore, and all our activities are in the hands of a few men. We have come to be one of the worst ruled, one of the most completely controlled and dominated governments in the civilized world. No longer a government by free opinion, no longer a government by conviction and the vote of the majority, but a government by the opinion and duress of a small group of dominant men.”

– President Woodrow Wilson

“There are two ways to conquer and enslave a nation. One is by the sword. The other is by debt.”

– John Adams, 1826

“The principle of spending money to be paid by posterity, under the name of funding, is but swindling futurity on a large scale.”

– Thomas Jefferson

“All the perplexities, confusion and distresses in America arise not from defects in the constitution or confederation, nor from want of honor or virtue, as much from downright ignorance of the nature of coin, credit, and circulation.”

– John Adams

“It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.”

– Henry Ford

“But when you recall that one of the first moves by Lenin, Mussolini and Hitler was to outlaw individual ownership of gold, you begin to sense that there may be some connection between money, redeemable in gold, and the rare prize known as human liberty.”

– Howard Buffett, Warren Buffett’s father and former U.S. Congressman

”Although gold and silver are not by nature money, money is by nature gold and silver.”

– Karl Marx

”There can be no other criterion, no other standard than gold. Yes, gold which never changes, which can be shaped into ingots, bars, coins, which has no nationality and which is eternally and universally accepted as the unalterable fiduciary value par excellence.”

– Charles De Gaulle, First French President

“If all currencies are moving up or down together, the question is: relative to what? Gold is the canary in the coal mine. It signals problems with respect to currency markets. Central banks should pay attention to it.”

– Alan Greenspan

All this “gold selling” (backed by the big financial insitutions and so on).

How many of these “gold sellers” actually have the PHYSICAL GOLD they have sold?

If asked for the DELIVERY OF THE PHYSICAL GOLD how many of these sellers could deliver?

Just asking…..

One interesting effect of this gold price slump is that all those government debts, expressed in real money, rather than “funny money” which can be created out of thin air, have suddenly got much bigger.

It’s not just government debts that gyrate in value when gold becomes a form of money: it’s everything else!! And therein lies one of the flaws of making gold a form of money.

If the price of gold relative to the price of everything else is allowed to fluctuate along with market forces, then the price of everything in your local supermarket would have to be re-priced every few hours. Of course that little problem was solved when sundry countries were on the gold standard by artificially fixing the price of gold.

But that detracts from one of the supposed merits of gold as a form of money, namely that its value is determined by market forces.

It’s not just government debts that gyrate in value when gold becomes a form of money: it’s everything else!! And therein lies one of the flaws of making gold a form of money.

It isn’t a flaw and it certainly would not require hourly retail price adjustments. That the price of gold has fallen vs. the dollar means simply that many people changed their preference from holding gold to holding dollars. It certainly does not mean that the purchasing power of gold fell.

When, as an example, British Sterling falls, say, 10% against the dollar, the price of Big Macs in Trafalgar Square are unaffected. The purchasing power of the pound hasn’t fallen; fewer dollar holders wanted pounds.

Mr Musgrave if you do not wish to be paid in gold – that is fine. And if you do not wish to trade with people who wish to be paid in gold – that is also fine.

Trade in some other commodity (silver perhaps?) with people who are willing to do business with you. If you really dislike gold, then you should certainly not be forced to have anything to do with it. And I AGREE with you that a gold STANDARD is a fraud – either gold is being used as money or it is not, a gold STANDARD just adds confusion.

However, just as government “STANDARDS” are bad so is ANY government messing with money. If there is one thing in monetary history that is clear it is that money must have nothing to do with governments.

The present seeking after “low interest rates” and efforts to prop up the housing market and “stimulate” the stock exchanges, are madness – utter madness.

By the way on “market forces” and the price of gold in terms of other things.

I do hope that the people the financial insitutions have been supporting to “sell gold” (to force down the price) actually have the PHYSICAL GOLD they are supposedly selling.

They are going to be asked to physically deliver the physical gold Mr Musgrave.

It would be so upsetting if the “great and the good” turned out not to have the physical gold they have supposedly sold.

I found this an intersting a persuasive explanation for why gold may have fallen. Of course we’ll never know. However – it’s worth a look I think.

http://www.alhambrapartners.com/2013/04/15/we-have-seen-gold-prices-act-like-this-before/

Sorry to be so late in catching up with your comment, Tim.

Yes, it’s definitely an interesting argument; however, I’m not sure it’s quite as persuasive as an explanation. Then again, GOFO and gold lease rates etc are not exactly familiar territory for me.

With that (rather large) caveat, a few thoughts:

1. First, I can’t see why heavy demand for borrowings secured by gold (i.e. gold repos/gold swaps) need translate into “a massive increase in supply on the paper markets.”

Snider says the “operational reality of a gold repo is a gold lease, charged at the forward rate (GOFO).” As I understand it, with a gold repo one party swaps their gold against the receipt of (say) dollars from the other party, with both agreeing to reverse the transaction at a predetermined rate and date. The effective rate embodied in those transactions is the GOFO (LBMA gold forward offered rate).

Presumably the recipient of the gold tries to earn whatever they can while it’s in their possession. Far as I can see, the choices are either lend out the gold for a similar period (i.e. a gold loan/gold lease), or sell the gold, invest the proceeds elsewhere and manage the resulting exposure to gold prices.

The latter is a risky proposition, requiring constant monitoring and highly developed hedging skills since simply fully hedging the resulting gold price risk effectively wipes out the carry trade return and renders the whole operation rather pointless. Maybe it does happen in sufficient volume to account for the sort of price movements Snider is highlighting, but before happily accepting that I’d want to see a fair bit of concrete evidence.

As for the alternative of lending the gold for a similar period, that certainly makes sense but does it really add to net supply? After all, the next borrower must repay the same amount of gold being borrowed (plus any interest) on the due date. So really, they’re faced with the same choice (and so on). In any case, gold rates (lease rates) have been mostly negative for some time at all maturities less than six months. So, if the repo in question is shorter term, the receiver of the gold under the original repo mightn’t even bother.

As an aside, gold lending can of course relieve liquidity squeezes in the gold market itself, but that’s not what we’re talking about here. Snider’s thesis is that in the scramble for conventional liquidity (dollars, euros, yen etc) as conventional collateral dries up, gold repos periodically come to the fore.

2. I’d also be really interested in seeing some details on where all this gold collateral is coming from. Are commercial banks really in possession of that much uncommitted gold? Alternately, perhaps (some) central banks are very generously making gold available to selected commercial (bullion?) banks so they can repo it out? I don’t know, but I guess it has to be possible. Certainly, the fact that gold lease rates now spend so much time below zero suggests something unusual is going on. Either gold repo demand is strong enough to push up GOFO enough to produce negative gold lease rates (which equal LIBOR – GOFO), or – maybe – some central banks are engaging in a new form of “bailout”.

What I’d really like is for someone truly knowledgeable about these arcane matters to pop in. The above makes sense to me, but we all know what they say about “a little knowledge” . . . .

Hmm.

Re point 1, I see your argument Ingolf. I myself was confused. Gold is not being sold, only used as collateral so why would it affect the cash gold market? Reading that article more closely, the authors seem to suggest that a whole bunch of sales due to REPO transactions results in a bit of a panic as investors are not aware of the meaning of these sales. This, thought, would be wholly unconvincing though given that this would simply show up as additional volume.

It seems that the more likely answer is simply that there are plenty of speculative and leveraged gold holders, holding with the view that there is a risk of significant bale out/inflation. When it appears that a more deflationary event is imminent, then sharp moves down ensue therefore.

With respect to your second point, I don’t beleive that central banks would have any particular cause to lend out gold for uses as collateral given that a whole heap of different government bonds are used for this purpose and their volume dwarfs that of gold. This said it doesn’t seem logical that the gold lease rates should be so low. Perhaps the answer could be that LIBOR is no longer a very good reference rate for the banks’ cost of funding. Perhaps the rate of interest on their reserves with the central bank might be better viewed as the opportunity cost given the vast quantities there?

Yes, it’s not exactly a transparent area, is it. Re LIBOR, I don’t know, Tim. You may be right but looking at a few charts things seem reasonable enough.

In any event, as we both seem to agree, even assuming Snider’s right about the volume of gold repos, his case turns on the existence of an effective transmission mechanism from there to heavy gold supply. If the recipients of the gold usually engage in carry trades, that would certainly do it.

As I said earlier, I guess it’s possible but I’d sure love to see some decent evidence.

A possible reason that gold fell so sharply could be that the gold market is almost unique, in that it is not supported, directly or indirectly, by any government or central bank

Michael, would you mind elaborating a little on why you see the gold market as unusual in this respect?

Ingolf,

Thanks for picking up what may have been a loose statement by me. Arguably, I was a victim of my own preconceptions, in that I was viewing gold as being a financial instument, rather than a commodity.

I believe that whilst gold may be manipulated, this is still unproven, whilst the share, interest rate, housing and currency markets are heavily influenced in different ways by government and central bank intervention.

If you are thinking of copper, lead, orange juice, etc you are correct, and I apologise.

No reason at all to apologise, Michael. As it happens, I largely share your preconception.

Even setting aside the word “manipulated”, though, wouldn’t you agree that gold is influenced by officialdom through central bank holdings and their net dealings?

Just a matter of curiosity, apart from the general effects of monetary policy, in what ways do you see the sharemarket being heavily influenced?

Yes, Ingolf, gold certainly must be influenced by central bank dealings. However, they do happen quietly, which could explain why I have tended to discount them.

I feel that the sharemarket is helped by (1) artificially low interest rates, and (2) QE, which is not dropped from helicopters, but rather goes to those such as the banks, who then “do their own thing” with it.

OK. Thanks, Michael.