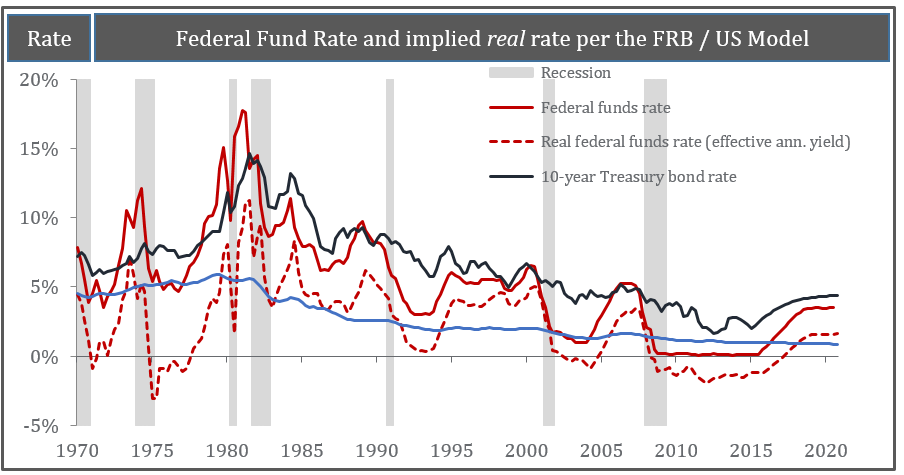

Despite zero-interest-rate-policy (ZIRP) and multiple quantitative easing programs — whereby the central bank buys large quantities of assets while leaving interest rates at practically zero — the world’s economies are stuck in the doldrums. The central banks’ only accomplishment seems to be an increase in public and private debt. Therefore, the next step for the Keynesian economists who rule central banks everywhere is to make interest rates negative (i.e., adopt negative-interest-rate-policy or “NIRP.”) The process can be as simple as the central bank charging its member banks for holding excess reserves, although the same thing can be accomplished by more roundabout methods such as manipulating the reverse repo market.

Remember, it was the central bank itself that created these excess reserves when it purchased assets with money created out of thin air. The reserves landed in bank reserve accounts at the central bank when the recipients of the central bank’s asset purchases deposited their checks in their local banks. Now the banks have liabilities that are backed by depreciating assets (i.e., the banks still owe their customers the full amount in their checking accounts), but the central bank charges the banks for holding the reserves that back the deposits. In effect, the banks are being extorted by the central banks to increase lending or lose money. The banks have no choice. If they can’t find worthy borrowers, they must charge their customers for the privilege of having money in their checking accounts. Or, as is happening in some European banks, the banks try to increase loan rates to current borrowers in order to cover the added cost.

In European countries where NIRP reigns, so far, the banks are charging only large account holders for their deposits. So, these large account customers are scrambling to move their money out of banks and into assets that do not depreciate. The scramble for high grade securities has resulted in some securities being sold at a premium (i.e., the customers will get back less than they invested).

How can this be? Well, the premium amount is less than the charge by the banks, so the large account customer is slightly less worse off. He loses somewhat less money. But this really does not solve the problem; it just means that the excess reserves are moved somewhere else, simply creating the same problem for a new set of banks that ended up with the money after the first group of investors ditched their cash for securities.

But that is not what the central banks want. The central banks want to force the commercial banks to lend money in order to avoid the excess reserve charge. They appear poised to increase the so-far-nominal cost of a half percent or less. If the central banks can charge a half percent, they can charge anything they wish and, given the Keynesian mindset that led to the insanity of negative rates in the first place, probably will do so.

What Interest Rates Are For

Negative rates violate numerous tenets of sound economics. For example, the basis of interest rates is consumer time preference, described by David Howden in an article written almost three years ago about the loss of Canadian manufacturing.

Time is a factor necessary for production, and unique in the sense that we cannot economically allocate it like other inputs. The choice of time is always “sooner or later” and never “more or less” (as is the case with other input factors). Interest rates help us determine how soon we should consume a good, or how long a production process should be. Low interest rates imply that the future is not heavily discounted. At a low rate you will be willing to wait a longer period of time to realise the enjoyment of consumption or the profits of an investment. High interest rates invoke the corollary — you will want to consume earlier, or employ production processes that pay off in as short a time as possible.

Dr. Howden goes even further to show how central bank production of money out of thin air in order to drive down the interest rate causes disequilibrium between borrowers, investors and savers. The very purpose of the interest rate in an unhampered economy, however, is to create equilibrium between these two groups.

Disequilibrium in the time structure of production (primarily an overinvestment in longer term projects), and an inevitable boom-bust business cycle that follows, results from the fact that real savings had not increased to provide the real goods necessary for the increased investments. First, businesses go bankrupt, then the banks, and then the population as a whole.

The Inevitable Bust

But can’t the central bank just print more helicopter money to save everyone? Unfortunately, no. More money cannot cure what too much money created.

Of course, an economy that has been thrown into disequilibrium by negative interest rates may display many weird anomalies before succumbing to the “crack up boom,” as described by Ludwig von Mises.

One early indication of loss of confidence in money is a commodity boom in precious metals. Prices rise faster and faster and production collapses. The public understands that the monetary authorities have no intention of reversing their negative interest rate policies and restoring sound money and banking. In a mad rush to save their wealth from total destruction, the public will start to buy what it hopes to be assets that will not depreciate. This sets off a huge boom in some asset categories; thus the “boom” portion of Mises’s “crackup boom” scenario. But the crackup follows on the boom’s heels.

The real pity is that the busts and crackups could all have been avoided if central bankers recognized that falling prices eventually create the conditions for a normal economic revival. Deflation is not a death spiral as the Keynesians believe. In a functioning market, the public’s demand to hold money will be satisfied when their reserves of money balances are sufficient in relation to the price level, when they are once again confident of the future, and when they are willing to invest for the long term.

Thus, the suppression of interest rates has been unnecessary and harmful. Nevertheless, expect more central banks to follow the early leaders — Switzerland, Sweden, Denmark, and even the European Central Bank itself — into negative interest rate territory. The crying shame is that it will not work and will cause great harm to hundreds of millions of people.

Source: https://mises.org/library/where-negative-interest-rates-will-lead-us