I came across this excellent report by Boone and Johnson from the Peterson Institute for International Economics on the mechanics of how the Eurozone sovereign debt crisis built up (hat-tip James Aitken of Aitken Advisors).

The report helpfully runs through the various policy options that the Eurozone leaders have, and runs through the likely consequences of default – interesting reading given the growing probability of some portion of this option being taken with respect to Greece at least. The writer at least believes that default and ‘an end to the moral hazard regime’ has now become the most likely option.

Cobden centre readers will enjoy the description of how it was the ECB’s repurchase operations that entrenched moral hazard throughout the Eurozone through the treatment of all sovereign paper as collateral from banks equally regardless of its creditworthiness.

There is also an up-to-date summary of the current net claims of all countries against each other, all guaranteed and monitored through the ECB, imbalances that are still building. Germany as of July was the largest creditor to the scheme at over Eur335bn. In gamblers’ parlance Germany’s decision over whether to throw good money after bad will determine the route the crisis will take next.

Things have moved so quickly it all seems quite out of date now that the guardians of the Eurozone have hatched their masterplan. Talk about smoke and mirrors! The EFSF is to be leveraged 5x by the ECB in order to reach a REALLY BIG NUMBER to recapitalise banks and calm debt markets while Greece begins default. This is printing through the back door on a massive scale. Of course we are by now used to the EU leaders doing whatever they want without our say so but this time, they haven’t even had the decency to tell us they are creating a E3.5trillion support fund from thin air and briefing this only to various journalists behind closed doors. It stinks.

Tim,

The problem is that some way has to be found to keep the Euro going, as a break up of the Euro would be catastrophic for the countries involved and the world economy; Any way out is going to involve some pretty unpalatable choices.

Indeed – there are no solutions that allow all parties to carry on as before. Hence, the policy makers are left with the unenviable position of making the least bad choice. This said, I firmly believe that it is never too early to start doing the right thing.

I disagree with you when you state that a break up of the Euro would be catastrophic for the counties involved and the world economy. This would depend on the nature of the breakup. Any movement towards appropriate risk-allocation and market-based incentives should be welcomed. Disruption is inevitable in any case.

In addition, I am not so fearful of the disruption of a sharp correction towards market-based incentives as many. My reason for saying this is that even if it were possible to devise a grand master plan under which a slow transition towards a better system were possible (which it isn’t), the practicalities of this are that no one policymaker holds complete sway over policy and the influences of each changes enormously from month to month. The implementation of any such grand plan, non-disruptive plan is therefore completely impractical as the result of this would inevitably be a series of short-term fixes designed to paper over cracks. This would make any future correction more serious. It also risks a complete loss of freedom of individuals as governments increasingly take charge. It is this that is the slide into the abyss rather than any effects of a short-term disruptive but long-term positive change.

Extreme political will to push though difficult but necessary changes inevitably lasts only a very short period of time. It is therefore wise during these periods not to put off until tomorrow what may be accomplished today since tomorrow invariably never arrives.

Tim,

I thought the short paper below from Barry Eichengreen was interesting. The argument is that however much it may be detrimental for the countries involved to stay in the Euro, it is near impossible for them to leave it. For the weaker countries, Such as Greece, this would mean massive capital flight and a consequent severe banking crisis. For the stronger countries, such as Germany, it would mean large appreciation of the currency and loss of export competitiveness. So realistically, even under the present dire circumstances, a break up is extremely unlikely.

What is more likely I think is a Greek default within the Euro and a large guarantee from the ECB of sovreign debt for those countries which are solvent. In the current recessionary circumstances, the ECB could afford to buy trilions of euros of bonds without this leading to inflation.

http://www.econ.berkeley.edu/~eichengr/can_euro_area_7-23-11.pdf

Dan,

Ambrose’s proposal to break-up the EMU into two regions, one with Germany and the other with France:

http://www.telegraph.co.uk/finance/financialcrisis/8755881/Germany-and-Greece-flirt-with-mutual-assured-destruction.html

http://blogs.telegraph.co.uk/finance/ambroseevans-pritchard/100012223/frau-merkel-it-really-is-a-euro-crisis/

John,

Thanks for the links, this is an interesting proposal and would seem to go some way to solving the Euro areas problems. However I think that any break up of the Euro is very unlikely, see my response to Tim below.

Thanks for the paper Dan.

I think you are right in what is the most likely policy outcome over the next few months. However, I do not agree that this would be a good outcome. I also believe that if this policy were followed, that either the weaker members would leave the Euro within a short time due to massive unemployment or that the strong members would leave through an appreciation that a permenent system of transfer payments is not in the national interest.

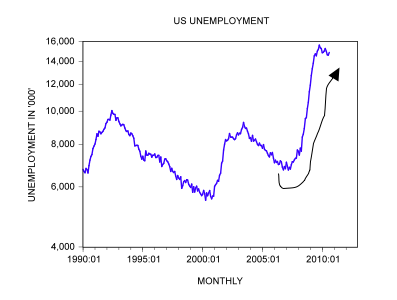

Firstly,this course of action would do nothing to solve the fact that Greece is uncompetitive. Without the public sector to take up the slack, unemployment would be 20%+ in Greece until wage deflation takes them back to the right level (I note that in Hong Kong, through maintence of the dollar peg, this took 6 years). I don’t think that the Greek people would put up with this and believe that Greece would voluntarily leave the Euro within a few years. The policy would be seen as oppression – quite literally there could be a revolution in Greece.

Secondly, the creation of money in order to prop up banks is just the sort of papering over the cracks solution that I refer to above. It essentially feeds the banks (and public sector periphery) at the expense of ordinary savers (who lose out through inflation). Regardless of whether CPI inflation is measured, there would be inflation relative to the amount that would be there in the absense of money-creation. In this way, savers subsidise uncompetitive exchange-rates and uncompetitive banks. This is not a policy for growth. It must be remembered that economic growth is nothing to do with measured GDP, but rather the process of capital formation. This is based upon the accumulation of voluntary savings garnered through the constriction of consumption such that these savings may be used to bridge a gap in time during which a capital good may be produeced that ultimately provides better and cheaper consumer goods in the future. This principle was introduced by Bohm-Bawerk and expanded upon by Jevons, Von Mises and Hayek amongst others. It is – in my view the fundamental building block that differentiates Austrian economics from monetarism and Keynsianism which have no theory of capital formation at their hearts. By definition therefore, a policy that expropriates private savings is anti-growth. It would therefore delay any recovery.

The fact that the Germans would be less competitive if their exhange rate rose is no reason not to allow it to move to a market level since the other side of this coin is that through its continued unnatural competitive position, Germany accumulates a surplus. This amounts to vendor-financing which is never sustainable. This just allows problems to build.

Yes, Greece would have a banking crisis if it left the Euro. Likely – without government intervention, this would result in a banking crisis globally. Is this something that authorities should looke to prevent? I don’t think so. I would argue that in the event of a banking crisis, that no capital is actually destroyed at all. If one thinks of capital as the sum of all the available goods and services that may be put to work – all the buildings, the cars, the machinery, the natural resources etc. All these stay in place. What the banking crisis does is to disconnect existing owners from these assets if they are unable to afford them on an underlying economic basis. The reconnecition of them occurs when new owners are able to buy them from the existing ones. Following the adjustment, the economy would be ready to grow again.

Policy-makers would argue that this would be an extreme handling of events. However, in the long-run we’re going to get there anyway – better to get it over and done with quickly so that capital can begin to be deployed properly again, rather than attempt to frustrate the process of price discovery.

I do not believe that allowing a bank run to occur would be a precursor to extremist policies since firstly, it would be upholding the principles of fairness in that those that took most risk would lose. Secondly, a quick readjustment of economic variables back to equilibrium would provide for more employment over a relatively short period of time. Revolutions tend to occur only after a long period of oppression (economic or otherwise) such that people are desperate enough to risk all in order to change their leaders. A short adjustment would be unlikely to cause this – the policies that you mention (money creation, bank bailout, expropriation of savings, high unemployment for a decade, continued growth in government, arbitrary decisions over which assets to support, capital transfer, capital controls??) that are more likely to cause a slide into extremism and that could sound the death knell to free markets.

Tim,

Firstly, I think that you make some excellent points on the banks. The contrast that I like to make on how to handle a banking crisis is between Iceland and Ireland in the financial crisis. The Irish government stood behind all the debts of its banking system, and as a result has an almost unmanageable sovereign debt and will struggle for years to come. Iceland however took the correct course of action, keeping the payments system going but allowing creditors to the banks who had taken the risk to be wiped out. The economy of Iceland is now growing at quite a fast clip and is well on the road to recovery.

Now, Greece is in an incredibly difficult situation. As you say they are uncompetitive and in the current regime must deflate to become competitive. Greece’s situation could be compared to one of the countries on the classical Gold Standard – Greece is effectively on a gold standard type regime with respect to the other Euro countries. But in the classical gold standard, a country always had the option of cutting ties to gold and floating the currency if it got into trouble; this could be done simply by suspending convertibility at the central bank. Things are much more difficult than this for Greece though. As Eichengreen points out, Greek banks and financial markets would have to stay closed for an extended period if Greece went back to the Drachma, due to the horrendous logistical problems of switching currencies. Shutting down the payments system for any length of time in an advanced economy such as Greece would lead to ruin in my view.

Therefore, it seems to me that the most likely, and least bad, option is for Greece to default within the Euro. The people won’t like the continuing austerity, but I believe they will eventually come to accept it when it is clear that there are no obvious alternatives.

I also think Greece will default within the Euro. I’m not sure if this is a good thing or a bad thing yet.

I think one of the other PIIGS is likely to default soon too.