“A man who wants to lead the orchestra must turn his back on the crowd.”

– Max Lucado.

So. Farewell then Jim Slater, who died earlier this month. We met Mr. Slater only once, at an investment conference at the height of the financial crisis in 2008. Just before going on stage we asked him what he was doing with his own money. He replied,

“I own index-linked Gilts in bearer form and I am holding them in a fire-proof safety deposit box.”

We doubt if he was joking.

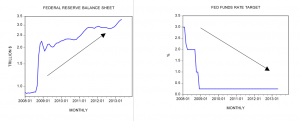

Seven years on from the collapse of Lehman Brothers, everything has changed, and yet nothing has changed. There is no longer a perception of panic. $14 trillion of central bank stimulus has seen to that. But at the same time, a predicament brought to crisis by too much borrowed money has been exacerbated by much more borrowed money: $57 trillion of it, according to the McKinsey Global Institute. Perhaps the most prescient commentator before the fall of Lehman Brothers was Tim Lee of pi Economics, who wrote the following back in November 2007, fully 10 months before the failure of a second-rate investment bank triggered a global credit crisis:

“There is little doubt, to my mind, that we are now at a defining moment in financial history, a time that, once it has passed will be referred by economic and market historians in much the same way as the Wall Street Crash of 1929 or the credit and banking crisis of 1973-4 are now.

“Unfortunately, as is becoming increasingly clear, this crisis is not really just about subprime mortgages. It is much more serious than that. It is the beginning of an inevitable realignment of credit and wealth with incomes and accumulated savings… subprime is merely the first part of the credit edifice to give way, rather than the whole story…”

For seven years and counting, only one question has really mattered to investors: inflation, or deflation ? Thus far, the answer seems to have been: inflation in financial assets, deflation or stagflation in pretty much everything else. It’s been difficult to get the macro right because central bankers have morphed from being referees in the game to being the key players, and with the ability to rewrite the rules, and continually move the goalposts, as the game plays out. The apparent dominance of central bankers over the free market should be of concern to anyone who expects the free market, at some point, to return with a vengeance. Meanwhile, as Mark Dampier suggests in his new book ‘Effective Investing’, just published by Harriman House,

“The question I like to ask fund managers is not what they think about the general economic climate but:

‘Are you still finding opportunities in the stock market today ?’”

This week’s ‘Economist’ magazine (‘Many unhappy returns: investing in a world of low yields’) points out that their answer should be ‘No’; the average American state or local government pension fund assumes it will earn a nominal annual return of 7.7% in future, according to NASRA, the National Association of State Retirement Administrators. Good luck to them. According to AQR, projected nominal returns on a typical American portfolio, given prevailing valuations in the stock and bond markets, are closer to 2%.

“The good news is that this is a long-term problem. Low returns are like a car with a fuel leak; it can still be driven for a while before it grinds to a halt. The bad news is that, precisely because this is a long-term problem, investors (particularly the politicians responsible for public pension funds) will be tempted to leave it to their successors. That will only make the eventual funding crisis even bigger.”

If the answer to Mark Dampier’s question is, truthfully, ‘No’, then the next question should logically be:

‘Are you sure you’re looking in the right market ?’

Investors, whether professional or private, have a tendency to succumb to home country bias. This problem will likely come back to haunt American investors because their home market is one of the more glaringly expensive. Robert Shiller’s cyclically adjusted p/e ratio for the US market stands at 26.4. Given that its long term mean stands at 16.6, that would tend to suggest that US stocks are trading at a roughly 60% premium to fair value. Two more reasons to be cautious on US stocks.. US interest rates are widely expected to rise next month. Not by much, but any kind of rise may mark the end of a three-decade secular bull market in rates. That has implications for all financial assets. And sceptics will have noticed two recent trends: a growing number of profits warnings on the part of large cap businesses internationally; and a growing tendency for US companies to ‘engineer’ better returns for their senior executives shareholders simply by buying back their stock at egregiously expensive levels. Stock buybacks conducted at a discount to book are value-enhancing. Buybacks conducted at whopping premiums to book, on the other hand, destroy shareholder value.

If the US stock market looks dangerously overpriced, where should equity investors be looking ? We think the answer is: in Asia, and more specifically in the likes of Japan, Korea and Vietnam. The shareholder return ratio in Japan, for example, stands at 36.6% – a derisory level compared either to Europe (71.4%) or to the US (82.9%). Japanese shareholders historically have been given a meagre slice of the pie. The good news is that their share of the pie is likely to go up. Both dividend payments and share buybacks as a percentage of profits in Japan are already on the rise, and we think they have plenty of room to catch up towards other ‘Western’ levels. The managers we invest with in Japan report that the change in Japanese corporate behaviour, especially amongst mid-cap businesses, is real. Since Japan also offers us highly profitable companies on p/e ratios of around 10x and price / book ratios of around 1, we simply don’t need to overpay to own the US market like the rest of the herd. (The prospect of more QE in Japan doesn’t exactly hurt – though we clearly prefer to have our currency exposure hedged, especially if US rates do rise.)

The Korean market is inexpensive too, trading on a p/e of roughly 10 and a price / book of around 1x. Vietnam is admittedly more of a ‘frontier’ animal, albeit one that’s widely expected to be recategorised as ‘emerging’ by the leading index provider in the fullness of time. As to valuation.. Vietnam has the lowest ratio of market cap to GDP in Asia, at just 30%.

So our answer to Mark Dampier’s question is: at a time when many investments are looking desperately mispriced, yes, we truthfully are finding attractive opportunities in the stock markets. We’re just looking at different stock markets compared to everybody else.

As always a very interesting article Tim.

I’m confident about South Korea and Vietnam.

If anyone wants to look at a real world example of a communism vs. capitalism showdown, a look at North vs.South Korea should surely convince the most deluded communist of why capitalism wins every time.

I was in Sydney last week and met a few vietnamese who had just finished study there. All of them intended to return to work in Vietnam with there skills once they establish residency/passport for Australia (Australia was a little boring for them and they have family pulls). This made me look up some stats. There’s approximately 25,000 studying in Australia at the moment – just from Vietnam. I’m not sure why they would value a ‘western’ uni education so highly, but that can surely only be positive for Vietnamese economy. Lots of young hard working people with english skills and ‘western’ experience, combined with ability and connections to apply those skills to a vibrant and energetic region. One sharp young man wanted to develop financial services in Vietnam, for example.

I know many companies in Japan are very well run and the stocks are cheap from a fundamental perspective, but I would be a lot more positive if the businesses were listed and operated from Singapore, for example, rather than Japan.

Have you listened to Kyle Bass discuss Japan? He makes a compelling bearish case, due to the levels of debt and the ageing population.

Do you think the government debt and subsequent interference could weigh too heavily on these businesses? When you look at total debts to GDP, both us and Japan do seem in competition on who can be the most financially insane.