Regulation – the hidden curse

byRegulations are nearly always introduced with the best intentions. In financial services, they aim to stop unscrupulous brokers and banks from ripping off the…

For honest money and social progress

For honest money and social progress

Regulations are nearly always introduced with the best intentions. In financial services, they aim to stop unscrupulous brokers and banks from ripping off the…

Please bear with a brief quote from a favorite author of mine. I promise it relates to gold. Having fought in World War I,…

Last week, the ECB extended its monetary madness, pushing deposit rates yet more negative. It is extending quantitative easing from sovereign debt into non-financial…

This article is from EDCAB.eu, with whom The Cobden Centre is working regarding a project for the European Parliament on digital currencies. Source: http://edcab.eu/blog/eu-tackles-virtual-currency-exchanges-wallet-providers The European…

Article by Marcia Christoff-Kurapovna. Source: https://mises.org/library/central-banks-and-our-dysfunctional-gold-markets Many investors still view gold as a safe-haven investment, but there remains much confusion regarding the extent to…

Source: http://www.alhambrapartners.com/2015/07/21/there-are-no-new-banks-dodd-frank-hits-five/ Today is the fifth anniversary of Dodd-Frank, the erstwhile government response to assure that the Panic of 2008 does not repeat. It…

The stories are all over the Internet. Governments are forcing us into a cashless society. Supposedly the pretext is terrorism, and the real reason…

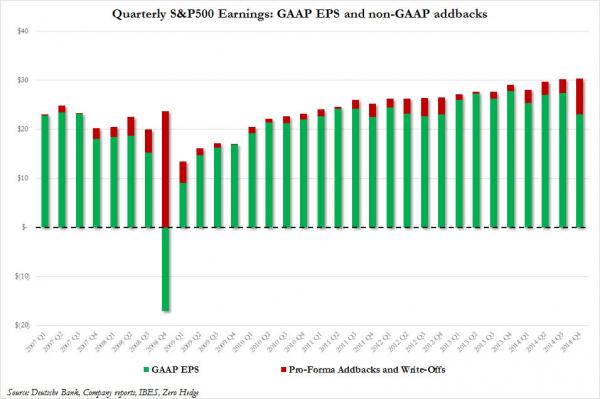

[This was first published at Zero Hedge here http://www.zerohedge.com/news/2015-06-08/non-gaap-revulsion-arrives-experts-throw-all-over-made-phony-smoke-and-mirrors-profi] One of the recurring stories on Zero Hedge has been the increasingly more blatant fabrication of…

I am sometimes asked what investors should look for if they are thinking of investing in a cryptocurrency. My initial reaction is that I…

[This piece appeared first here http://www.epictimes.com/richardebeling/2015/04/when-the-supreme-court-stopped-economic-fascism-in-america/] There was a time when the Supreme Court of the United States defended and upheld the Constitutional protections…