The Deadliest Virus

byThe deadliest virus is the institutionalized coercion which lies in the very DNA of the state and may even initially permit a government to…

For honest money and social progress

For honest money and social progress

The deadliest virus is the institutionalized coercion which lies in the very DNA of the state and may even initially permit a government to…

In economic terms, war and pandemic are the same without even evoking imagery of the virus as an invisible enemy or of a long…

The powerful forces of bank credit contraction are at the heart of a rapidly evolving financial crisis in global derivatives, whose gross value is…

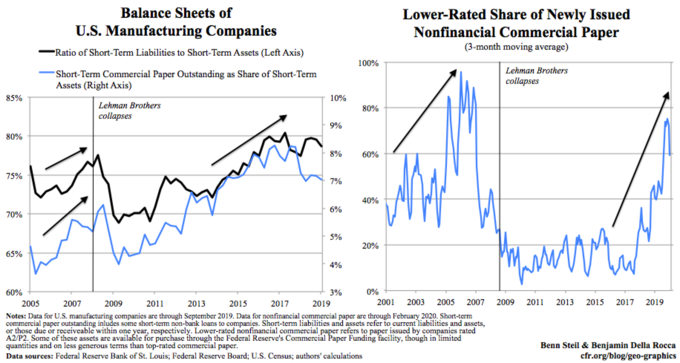

By Benn Steil and Benjamin Della Rocca Acknowledging the enormous threat to jobs and incomes posed by the coronavirus epidemic, the Federal Reserve on…

Despite three Federal Reserve rate cuts, leveraged loan credit quality is rapidly declining Covenant-lite issues now account for more than 80% of US$…

Russia dumped 84% of its American debt,” blared a July CNN headline. Russian central-bank head Elvira Nabiullina said the sales were just part of “diversifying the entire structure…

Is the global economic recovery over? That is the question investors are grappling with just as Q1 earnings season – the best since 2011 with its…

You’ve heard the axiom “History repeats itself.” It does, but never in exactly the same way. To apply the lessons of the past, we…

“There is no simple, painless solution. The world has to reduce debt, shrink the financial part of the economy, and change the destructive incentive…

The latest BIS quarterly report can be found here: http://www.bis.org/publ/qtrpdf/r_qt1509.htm Relative to the IMF, World Bank and national central banks around the…