It is notable that on a periodic basis, complaints are made in the press by concerned individuals, politicians, journalists etc. about the lack of bank lending to home owners, small businesses and others. Loans are either priced too high or simply not available. Small business owners complain they are starved of necessary funds and individuals cannot buy their first home. House prices continue to fall due to a lack of liquidity and relative inactivity in the housing market. The crosshairs of blame are centred squarely on the banks.

The approach is typically to bemoan the lack of lending and suggest that the Government should “do something about it”. Rarely do these commentators turn introspective and consider the question “why”. Why are banks restricting lending and requiring more onerous terms than during the boom times? To ask the question is to answer it. We are not in a boom, and leaving aside the Government’s arbitrary definition of recession, the economy has not yet recovered. But obviously the banks must lend – this is how they make money. If banks do not lend they go out of business.

Banks still have a significant amount of high risk debt on their books that needs to be liquidised. Until this debt is repaid there is a limited supply of funds available for new loans. Given the law of supply and demand, the cost of these new loans will be higher. Furthermore, given the riskiness on the banks’ loan book, the terms will need to be restrictive so that banks can reduce their risk profile. This is, of course, the type of activity we should expect in the recovery phase generally. That is, businesses liquidating malinvestments, taking losses, and should the business survive, making more profitable but less risky investments in the near term. Banks are not behaving differently from other businesses, in this regard.

However, there is another factor affecting banks appetite for lending to businesses and individuals: the Government. It has been reported lately in the press that British banks have been the largest purchaser by far of Government debt in the past six months. Of £39.8bn issued, British banks have purchased £36.2bn. £36.2bn of bank lending going to the Government is £36.2bn less available to be lent to the private sector. As the Government soaks up the supply of cheap credit this in turn increases the cost of this credit to the private sector. Given the choice between a nominally risk-free loan to the Government and lending to a risky small business, it is obvious which borrower the banks will prefer.

This is indicative of the general irrationality of government. On the one hand to insist the banks start lending and on the other hand, to take all the available funds for themselves. It is clear that government cannot “kick-start” the economy, they can only slow it down, dragging out a recession for so long that few can remember what a boom feels like.

On the other side of the equation, it is likely that demand for bank lending has fallen. This makes sense since if businesses are conducting the same risk reducing policies as banks (liquidating malinvestments and taking losses) then their requirement for bank finance would be lower. Additionally, businesses would seek to fund from equity rather than debt in order to reduce the riskiness of their capital structure. Ultimately, once businesses and banks alike have reduced their risk profile to a more sustainable level, the quantity of debt demanded and supplied will increase.

However, if all this is the case, why is it that certain politicians are demanding that banks increase their lending? It is for two broad reasons. On the one hand, they feel the need to be seen to be doing something. This is to satisfy their various constituents (in this case it seems to be Small and Medium-sized Enterprises – SMEs – and the voting public). The second reason is because they appear to be ignorant of economic reality (wilfully or otherwise) and are certainly entirely ignorant of the concept of risk as it pertains to both banking and business.

As noted above, the economy needs to be cleared of malinvestments or in other words, unprofitable product and service projects. Capital (in the form of bank credit) needs to be redirected from these projects towards the most efficient use of these funds. This occurs once these projects are sold off and losses taken, by the business or bank or both. New loans will be made for lower risk projects and priced accordingly relative to the riskiness of the project and/or organisation managing the project. As SME’s have shallower pockets than large organisations, naturally the price of credit that SMEs are offered will be higher, with more restrictive terms. In some cases, if the bank’s appetite for this particular risk is insufficient, credit will not be extended at all. This is rational behaviour.

The Government wishes to short-circuit this process and follow a political process for allocating capital and disregard the credit risk process. This will result in an irrational allocation of capital, with funds directed by the Government towards an inferior place for it, one chosen by the Government rather than the market. Thus the pricing for the credit will be lower than that dictated by the market, leading to a shortage of credit in other areas (say for first time mortgage borrowers), likely requiring further government intervention in the future. Furthermore, projects that were previously unviable may instead of being liquidised continue to tie up scarce resources. Thus the spectre of “zombie” companies, feeding on the lifeblood of potentially healthy and profitable projects. This is not withstanding the distortion of the banks’ risk profile, possibility contributing to further financial instability in the future.

Thus the Government introduces further instability, uncertainly and inefficiency into the economy. This cause of action is unsustainable and will result in capital consumption while retarding the recovery. Already, the Bank of England is warning that the economy will remain depressed for a further three years. This does not inspire confidence in either the Bank of England or the Government. Government handling of the initial crisis has given us a prospective seven years of recession. This is astonishing by historical standards but was predictable based on an Austrian economics analysis.

The reason this (unofficial) recession is set to continue is primarily down to the actions taken by the Government and its agency, the Bank of England. On the one hand, raising taxes effectively slays the goose that lays the golden egg. On the other hand, quantitative easing has resulted in an insidious transfer of wealth from the population at large to the banks, making people in general, poorer. The banking bail-out represents a reward to banks for their excessive risk taking and incentivises them to continue their excessive risk taking in the future. This is beside the fact that these bail-out funds support the malinvestments in the economy and delay their liquidation, thus drawing the recovery out further and further into the future, as Mervyn King has confirmed for us.

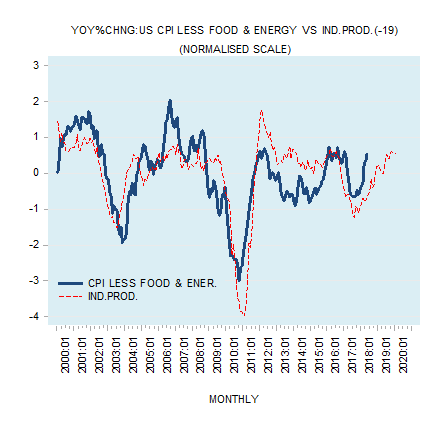

We can see clearly how the Government/BoE recovery plan has failed. GDP growth has sputtered, manufacturing is on the slide, housing market activity is depressed, consumer spending is down and inflation is growing faster than income. We are getting poorer, which is precisely the result we should expect based on a firm understanding of basic economics. This understanding appears to elude the Bank of England which sticks stubbornly to its low interest policy. Low interest rates are, ironically, one of the impediments to increased bank lending, not withstanding its negative effect on the recovery process generally.

There is no need to wait a further three years for recovery. The answer is for the Government and the Bank of England to get out of the way and cease their obstructive activities. This means the Government reducing spending and taxes, and the Bank of England to cease its interest rate manipulation, alongside an end to fractional reserve banking. This will force banks to curtail risky lending, reduce the likelihood of the damaging business cycle and end the socialisation of risk and losses.

Insightful piece. Intelligible and engaging for economists and non-economists alike.

Robert Sadler repeats the standard Austrian idea that there are an excessive number of “mal-investments” in a boom and its aftermath.

The first flaw in this idea is that hundreds of businesses go bust every week and hundreds of new ones start up, regardless of whether an economy is booming, stable or collapsing.

Second, I’m sure the number of businesses which will not be viable in the long term expands in an unsustainable boom. But they go bust come the recession.

So whence this idea that there are a particularly large number of “not viable in the long term” businesses hanging on once the worst of a recession is over?

Ralph,

I knew that you would be disappointed with my article but I actually think your comment supports my arguments. I agree businesses go bust no matter what the state of the economy but your assertion that unviable businesses expand in an unsustainable boom and go bust in a recession is actually central to my argument. My further point is that Gov’t acts to slow the process of liquidation with all kinds of “assistance” financial or otherwise. This “assistance” gums up the works, so to speak, so that the process of unwinding these projects takes longer than it should.

Thus, we have more unviable businesses hanging on that we otherwise should. Speaking anecdotally, it is actually my job to liquidate or otherwise deal with struggling businesses, many of which would be long gone if not for the BoE’s artificial low interest rate policy. Certainly, certain banks, like RBS and Northern Rock would not exist if not for government assistance. Is it ethical or economically viable that these failed organisations should be allowed to continue in operations, at the expense of generally responsible taxpayers?

It is impossible for me to debate with you in detail on this in a comment Ralph but I suggest you read America’s Great Depression by Murray Rothbard. The arguments Rothbard makes in that book against government intervention are completely relevant today.

Robert, I quite agree that government / central bank interference with interest rates is not desirable. I actually devoted a post on my blog to this point:

http://ralphanomics.blogspot.com/2010/12/interest-rate-adjustments-are-useless.html

I also agree that government should never support what were popularly called “lame ducks” a decade or two ago: i.e. failed businesses. And that includes banks. Walter Bagehot said something to the effect that the best way to stifle an efficient bank is to give artificial support to an inefficient bank. He was right.

That leaves businesses which do NOT receive government support. And it’s here that I don’t get the Austrian claim that an excessive number of loss making businesses hang on after the worst of a recession is over.

Ralph,

In my view, this could possibly happen with indirect government support. In other words, the government lowers the cost of funds for banks so that banks can afford to make lower interest rate loans to SMEs. This seems to be the strategy that the Gov’t and BoE were pursuing but as we have seen it is not working as well as they would like. Larger businesses with deeper pockets seem to be benefitting but not SMEs.

This is because the cost of funds is only one factor in whether or not a bank makes a loan. Another more important factor is the risk that the bank will not get its principal back. If the bank views the risk of loss as too great it doesn’t matter what the interest rate is – the bank simply won’t make the loan. And so the Gov’t is now trying to strong-arm the banks into making loans.

“£36.2bn of bank lending going to the Government is £36.2bn less available to be lent to the private sector. As the Government soaks up the supply of cheap credit this in turn increases the cost of this credit to the private sector.”

This is simply not the case- we are in a liquidity trap situation where there are excess unused savings in the economy. Therefore government borrowing is not in any way “crowding out” the private sector, as it would do normally. All it is doing is giving those excess savings somewhere to go, which is a good thing!