Since the Great Financial Crisis started (in truth, since well before), we have unwaveringly maintained three main tenets in relation to how one should deal with the aftermath of a credit-driven, mass misallocation of resources.

Firstly, we have said that, even if we did accept, arguendo, the trite macroeconomic mumbo-jumbo of over-aggregation, that tired old, maintenance-of-spending-at-any-cost, Keynesian game of trying to compensate for the overstretch of one particular ‘sector’ of the economy by passing ‘the bad, or depreciating, half crown to the other fellow’ is most likely to tangle us in an inextricable knot of surindebtedness if the ‘fellow’ is a governmental body. We say this, since the specious initial advantage of the state’s temporary ability to ignore the imperatives of accounting logic is doomed to be overwhelmed by the legal intractability associated with that same entity’s eventual financial exhaustion. Furthermore, this mere procedural failing is always horribly compounded by the dilution of the sense of direct responsibility which accompanies its involvement in any plight in which the relevant country lands itself.

Secondly, we have stood foursquare behind the idea that all the losses are actually incurred during the heady euphoria of the Boom, that the Bust is nothing more than the overdue recognition of those mistakes, and that to procrastinate thereafter in their acknowledgement is not to avoid the pain, but to exacerbate it in much the same way as a sufferer from a cancer can do himself nothing but harm by trying to delay the awfulness of the therapy which sadly must await him.

Thirdly, it has been our avowed belief that, contrary to the accepted wisdom, there are very few useful macro solutions to such a condition, but only micro ones; that recovery is built one job, one company at a time, from the bottom up.

Therefore, the most beneficial role for Leviathan is not some crazed, Frankenstein process of pulling levers and administering potions in some swivel-eyed, Gene Wilder fashion, but is one of expediting the renegotiation of now-unfulfillable contracts; of impartially overseeing a just transfer of assets from the failed to the well-founded; and of ensuring as few scarce resources as possible—in this time of unexpected penury—are pre-empted by the dead hand of the bureaucracy and, hence, are made available to the putative builders of a new, more prosperous tomorrow.

In all of this, we have been generally cynical of the ability of politicians to deny themselves the chance to carve their effigy on an imaginary Mt Rushmore of interventionists. We have been even more deprecatory of the nomenklatura of would-be Plato’s who advise them, those ’socialists of the chair’ who blindly fill their pink column inches with the ludicrous argument that the only remedy for the failure of government interference is more interference. We have been vehemently opposed to the machinations of central bankers—the ultimate succourers, when not the original seeders, of the Boom—who continue to frame every response in terms of the provision of liquidity to their precious cartel of institutionally parasitic, fractional reserve banks.

Despite this, it has been hard to suppress the faint fluttering of a hope lately freed from its hard chrysalis of doubt by the integrity of some members of the northern European political class and their nominees within the Heart of Darkness of the central bank itself.

Germany—with both tacit and expressed support from among the Dutch, the Finns, the Slovaks, and others—has wrestled itself close enough to doing the right thing—to writing off much of the debt; to making the imprudent private owners and creditors face their responsibilities; and to insisting on guarantees of future good housekeeping from the incontinent debtors—to merit our applause, even if its courage eventually does fail it, or the temptation to take the road to hell along which everyone else is frantically pointing finally does prove too hard to resist.

However, any sense of the victory we entertain in this critical war of ideas—albeit four years late and several trillion dollars short—has to be tempered greatly by the awful truth that two of the major central banks have already succumbed, once more, to their liquidity fetish, while a third is patently ravening for the chance to overcome the present domestic impediments to further action.

One of them, the ECB, is slowly transforming itself into a Fed—over the careers of ex-Bundesbankers perhaps, but nonetheless inexorably so.

Believe, if you will, that all such measures as those announced this week are ‘temporary’—only to be countenanced for the duration of the emergency—and, as our New York friends say, I have a bridge to sell you in Brooklyn.

Yes, it is true that interbank lending has frozen, that the vast apparatus of sovereign finance is creaking alarmingly, and that real money supply growth in the Zone is hovering just above the zero bound. Of these, however, only the third is a potentially justifiable field for central bank intervention in extremis.

The first is a consequence of the long-suppressed mistrust of one another’s balance sheets being expressed by the banks themselves; a fear which could be dispelled overnight if they would each do no more than is required of any public corporation, namely, to produce an honest set of accounts, even if this would be to undertake an exercise in triage—of the merciless sorting of the weak from the strong. To recognise its origin is already to point to where the cure may be found—extended repo operations and expanded bond purchases do not lie along that way.

The second handicap is the legacy of long years of populist vote-buying whereby venal politicians have far too liberally dispensed a morally corrupting patronage, not by having to undertake the invidious task of clearly identifying the winning net recipients of tax monies from the losing net payers standing beside them at the hustings, but by recourse to the seemingly painless expedient of borrowing funds which are never intended to be repaid and which are, in great part, the result of inflationary credit creation on the part of the same central and commercial banks who are now so threatened by the fall of all these democratic Bourbons. Again, to make this diagnosis is to indicate what form the remedy must take and to show that the prostitution of the central bank, so as to maintain the status quo ante, will prove futile, if not fatal, to the patient

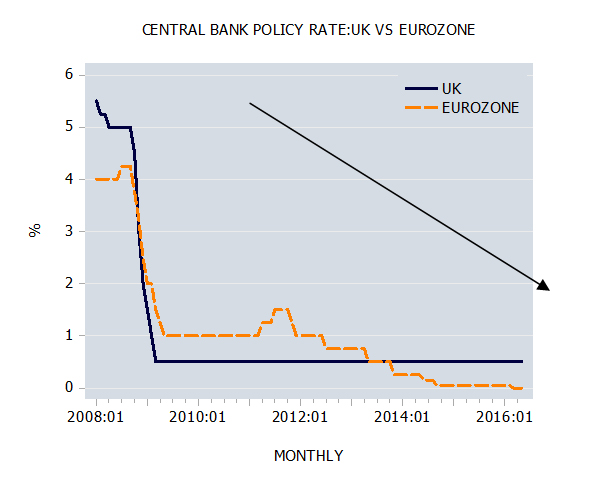

As for the Bank of England—well, yes again, real money supply has been running at a negative rate in the UK for some good few months past, dragging activity lower as it has. Yet a very good part of this real contraction is because the Bank has also managed to ignite a nasty rise in prices in violation of its rather open-ended mandate to moderate these over a self-determined and highly elastic ‘medium-term’.

As we have said before, the fact that the UK still manages to run a near-record trade deficit amid a severe recession and during an ostensible private sector credit crunch, despite a 25% drop in sterling’s real effective exchange rate such as to take it to a level only matched during the IMF crisis of the mid-70s Labour administration, is testimony both to the fact that the overall squeeze is not so intense as it seems and to the failure of all this macro-meddling to restore a semblance of competitiveness to a hollowed-out nation.

Where the leakage occurs, of course, is in the realm of the state where, for all the gnashing of teeth and tearing of hair about the ‘austerity’ programme, spending continues to rise, with the change in the state component of expenditures in Q2 outstripping that of households for the fifth quarter out of the last six. Total state outlays are still making new record highs, both outright and as a proportion of non-state GDP—that latter ratio now bumping up against the 60% mark, no less.

So it is all very well for Mervyn King to bleat about facing the most severe financial crisis since the 1930s, or to casually dismiss the cries of the thrifty that their livelihoods are being crushed in the vice of rising prices and falling returns to capital, but it is he and his predecessors, together with the political masters they serve, who have led us into these straits, by dint of their unshrinking embrace of a perverted orthodoxy of inflationary entitlement—of the entitlement of welfare recipients to their doles, of office-seekers to their votes, and of inveterate financial gamblers to their place at the tables of the state-sponsored, state-regulated, and state-underwritten casino.

Mr. King’s response to all this? Why, again to make it easy for the state to spend more and difficult for many of the most vulnerable elements of the nation to spend as much. Bravo, indeed!

So, while Chairman Bernanke can, for now, only threaten to increase the disruption he causes to the market’s pricing signals and to its ability to allocate resources optimally over time, his peers are already at work doing much the same mischief.

Caught up with the demands of their real dual mandate—that of keeping the ruling class happy while looking after the interests of their cabal of big bankers—few of them will stop to listen to what businessmen are telling them, though the message is being broadcast in the most clarion of tones.

Take the most recent Duke University/CFO Magazine quarterly survey of senior US executives as a case in point.

Asked to list external concerns in order of importance, the perennial question of sufficient demand for the firm’s products came top, but a clear second place was secured by the category ‘Federal Government agenda/policies’ – aka, REGIME UNCERTAINTY!

As for internal worries, the ability to maintain margins was top, the cost of health care, second, and the ability to forecast, third—over to you, Mssrs Bernanke and Obama, once more, for creating and fostering such extreme REGIME and MARKET UNCERTAINTY!

And the result of all this? Exactly what we showed in graphical form and briefly discussed in our last edition:-

A third of CFOs say they will not deploy excess cash this year, because they want to retain it should credit markets tighten. Twenty-nine percent say they are hoarding cash due to economic uncertainty, and 31% say they don’t have any excess cash to spend.

More worrying still for all those executives and traders who keep telling us that while business in the Old World may be slow, Asia will keep firing away and so save their bacon, the separate respondents from that particular region also manifested an uncharacteristically subdued tenor. We quote as follows:-

Optimism about the regional economy in Asia (not counting China) fell, with optimists and pessimists now evenly balanced. Last quarter, optimists outnumbered pessimists by two to one. In China, 69 percent of firms have grown more pessimistic about the economic outlook.

The top internal concern among Asian CFOs is difficulty in planning due to extreme uncertainty, working capital management and employee morale. The top external concerns in Asia are global financial instability, intense pricing pressure and weak consumer demand. Chinese CFOs also worry about government policies.

QED

But, carry on regardless! The present approach has been so successful that while one in ten Americans with a full-time job lost it in the slump, barely one in six of those unfortunates has found similar work since, leaving the total at 2000 levels and its fraction of the population at 1975 and 1983 recessionary depths, despite the intervening incorporation of women into the workforce. As for manufacturing—supposedly doing well on the cheapest dollar of the modern era—almost one quarter of the hours worked here were lost from the local maximum of 2006, of which, again, less than a sixth have since been replaced, leaving total hours fully a third below the stationary average of 1984-2001, and still stuck where they were in St. Roosevelt’s bleak 1940s!

Meanwhile, the 3mma of US NAPM new orders has dipped below the 50 watershed for the first time since the crisis, an event which has historically signalled a further deterioration over the succeeding six months in 70% of cases, and an ill omen we must interpret in light of the fact that the magnitude of the last few months’ fall in this component has only been exceeded three times in the past century—in 1974/5, 1980, and in 2009 itself.

Even in Germany, 2009-10’s impressive growth in factory orders has begun to peter out to the point that there has been little further sustained growth so far this year. Meanwhile, at the other end of the world, a PMI of Korean orders languishes at a 2-year low, while exports of capital goods from Taiwan have not been this weak since early 2010.

It may be too much to say that the wheels are coming off the recovery, but they are certainly beginning to wobble.

I have been led to beleive that VAT income is part of GDP? since VAT went up 2.5% growth in GDP has never passed 2.5% so surely we are in a reccession and there is no recovery to protect by printing money, even if this would protect it.