Most people — from young to old and from all ends of the political spectrum — are united by a common bond. The idea that banks are deserving of taxpayer support is viewed as morally repugnant to them. Business owners see bank bailouts as an unfair advantage that is not extended to all businesses. Those typically on the political left see it as support for the establishment, and a slap in the faces of the little people. Those more at home on the political right see it as just another form of welfare: a wealth redistribution from the hard working segment of the population to the reckless gambling class of banksters.

Despite this common disdain for bankers, there is considerable disagreement on how to deal with them. One group sees less regulation as the solution — letting market forces work will allow the virtues of prudence and industry to prevail. This formulation sees these same market forces as limiting firm size naturally to evade the “too big to fail” issue, through many of the same incentives that foment competitive economic advancement.

Another group sees the solution as more regulation. The natural tendency in business, according to this group, is for large monopolies to form. As companies grow in size, they gain political influence as well as an aura of indispensability. The consequence is that not only will a company come to be seen as too big to fail, but it will also be politically influential enough to seek such recourse if troubles surface.

Like most answers, the truth lies somewhere in the middle.

The first group correctly notes that there are two specific drawbacks of increasing regulation. On the one hand, “one size fits all” regulatory policies (such as is commonly the case on the Federal level) are rarely capable of handling the intricacies and dynamics of business. They also have the effect of relaxing the attention individuals and businesses afford to their own behavior. Under the pretense that the state has enacted wise regulations, individuals see little need to actively monitor companies to make sure they behave in a responsible manner. Businesses too succumb to this mentality. By abiding by the existing regulatory regime, they take solace in knowing that any attack on their integrity can be brushed aside as an attack placed more appropriately on the failures of the regulating body.

On the other hand, increased regulation breeds the problem of what economists call “moral hazard.” An activity is morally hazardous when a party can reap the benefits of an action without incurring the costs. The financial industry is very obviously afflicted with moral hazard today.

Banks and other financial companies have largely abided by the law. I would venture a guess that there is no industry more heavily regulated than the financial services industry, and no industry that spends more time and resources making sure that it complies with this complex regulatory maze. Capital levels must be maintained, reporting must be prompt and transparent, and certain types of assets must be bought or not bought. Banks following these regulations get a sense that they will survive, if not flourish, provided they work within the confines of the law.

However, it is increasingly evident that the financial regulations put in place over the past decades are woefully inept at maintaining a healthy financial industry. In spite of (or perhaps because of) all these regulations, a great many companies are, shall we say, less than solvent. So, who is to blame? It would be easy to blame the companies themselves, except that they did everything that the regulators told them to do.

Why not at least consider relaxing regulations? Doing so would have a two-fold advantage.

On the one hand, businesses would be more obviously responsible for the instability they have now created. On the other hand, without regulations, more reckless or clumsily managed companies would have gone out of business already, lacking the benefit of a regulatory “parent” scolding them for their mistakes. The result would be fewer unstable businesses, and more attention to the dangers of one’s own actions.

I previously mentioned that both sides are correct to some degree, implying that those calling for more regulation had some merit to their arguments. And this is indeed true. However, to paraphrase Inigo Montoya, when they use the word “regulation,” I do not think it means what they think it means.

It is true that not all companies play on a level field. In the financial services industry, and particularly in the banking sector, this is especially apparent. Banks are granted a legal privilege of “fractional reserves.” The result is that banks behave in a way which is fundamentally different from any other type of business, and which is easy to misdiagnose as “inadequate regulation.”

A depositor places money in his bank. The result is a deposit, and the depositor has a claim to this sum of money at any moment. One would think that the bank would be obliged to keep the money on hand, much in the same way that other deposited goods — like grain in an elevator — must be kept on hand. The law begs to differ. Banks are obliged to keep only a portion, or fraction, of that deposit in their vaults and are free to use the remaining sum as they please. Canada and the United Kingdom are examples of countries where there is no legal requirement for a bank to hold any percentage of that original deposit in its vault. In the United States, if a bank has net transactions accounts (deposits and accounts receivable) of less than $12.4 million, the reserve ratio is also set at zero. This differs greatly from grain elevators, where the law strictly states that the elevator owner must keep 100 percent of the deposited grain in the silo.

There are two results of the practice of fractional reserve banking, neither of them positive for the average person.

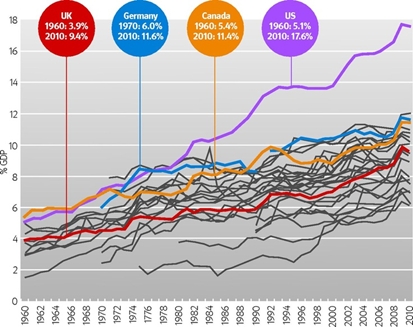

First, banks grow larger because they have access to a funding source that would otherwise not be available if they conducted themselves by the same laws as other businesses. When commentators say “banks are different,” there is truth in the statement. They have a legal privilege that enables them to grow in scope beyond that which they could naturally. This also explains why many banks, and financial services companies, come to be viewed as too big to fail.

Second, banks become riskier. Every time a deposit is not backed 100 percent, the depositor is exposed to the possibility of not getting his deposit back in full. If a bank uses his deposit to fund a mortgage, and the borrower defaults and cannot repay the bank, there is a risk that the original depositor will lose some of his money. A more common case is a bank run, in which many depositors try to withdraw money at the same time. The result will be insufficient funds to simultaneously honor all redemption demands. This occurred with various banks in Iceland, Ireland, Britain, and Cyprus over the last four years.

Few people worry about this latter problem, however, because of the former one. Since banks have become too big to fail, we are assured that if one goes bankrupt, we as depositors do not stand to lose personally. The government has pledged implicitly, or even explicitly through deposit insurance, that it will step in and bail out the irresponsible actors.

The result is the confusing state of affairs that we have today with two sides both arguing for the same thing — banking stability — via two diametrically opposed means. The “more regulation” camp is pitted against the “less regulation” camp.

A solution

These two camps are not mutually exclusive. We can solve the problems of moral hazard and “too big to fail” in one fell swoop by ending fractional reserve banking.

By ending this legal privilege, we eliminate the ability for banks to grow to such inordinate sizes. By abiding by the same legal principles (or “regulations,” if you will) as any other deposit-taking firm, banks are not unduly advantaged. If banks shrink in size, the “too big to fail” doctrine is eliminated, or at least greatly reduced. This means that depositors and bankers will realize that if a loss occurs to their bank, they personally stand to lose.

The risk of loss is a great force in removing moral hazard. Remember that it only arises when one person’s ability to gain is not constrained by the threat of a loss. Cognizant of ensuing losses, depositors will demand that their banks adhere to more prudent operating principles, and bankers will be forced to meet these demands.

The critics worried about “too big to fail” are right. We do need more “regulations,” in a sense. We need banks to be regulated by the same legal principles regarding fraud as every other business. The critics worried about moral hazard are also right. We need fewer of every other kind of regulation.

Repairing a broken financial system does not have to be hampered by irreconcilable political differences. Recognizing the true issues at stake — legal privilege and unconstrained risk taking — allows one to bring together advocates of widely differing solutions into one coherent group. Getting bankers to agree to all this is another story.

This article was previously published at Mises.org.

I agree that fractional reserve should be abolished. However, there is a problem with David Howden’s suggestion that ALL DEPOSITORS should bear the loss when a bank makes silly loans or investments. The problem is that some depositors specifically want a way of storing money in a 100% safe manner. Moreover, some entities have a legal obligation to store money in a 100% safe manner (e.g. lawyers looking after clients’ money).

Plus, I think that having somewhere store money in a 100% safe fashion is a basic human right: particularly for the financially unsophisticated.

The solution to that problem is phenomenally simple: give depositors a choice between two options. First they can have their money, or some of it, stored in a 100% safe fashion (e.g. lodged at the central bank) where it will not be loaned on, i.e. not put at risk. Second, they can let their bank lend on or invest their money, in which case, as David suggests, the depositor carries the risk when it all goes wrong.

Re David’s suggestion that making depositors bear losses will force banks to “adhere to more prudent operating principles”, my answer is “not necessarily”. Moreover, there is no need for banks to be particularly prudent. That is, if a depositor wants their bank to put their money into for example a unit trust that specialises in dodgy South American gold mines, why not? The risk will be high, but so too will the return be high. I’m all in favour of people taking big commercial risks, if that’s what they want.

I also don’t see why abolishing fractional reserve stops banks becoming BIG BANKS, and I don’t see any need to stop them becoming big. The beauty of making depositors bear the loss when things go wrong is that the stake that depositors then have in a bank is no longer a SPECIFIC SUM OF MONEY: it’s more in the nature of a shareholding. And if the bank does badly, the value of that stake just drifts downwards. That’s a huge difference to the current system under which banks suddenly realise they’ve run out of cash and everyone panics.

I.e. under full reserve, banks just can’t suddenly go bust. So there’s no harm in letting them grow relatively big.

Incidentally the above system where depositors have a CHOICE as to what their bank does with their money is advocated by Laurence Kotlikoff and Positive Money.

“I think that having somewhere store money in a 100% safe fashion is a basic human right”

Ah, human rights!

Nothing in this world is 100% safe. Your 100% reserve bank might burn down, or robbers might make off with the contents of the vault. The government might be overthrown in a military coup, and the central bank abolished.

People who want safety approaching 100% can put their cash in safe deposit boxes, or in a secret vault in their own homes. But 100%? That doesn’t exist in the real world, human rights be damned.

Besides, even in a dreamland where you can somehow have 100% protection for the nominal value of your savings, what good is that if the central bank has the power to reduce the real value of your savings towards zero?

OK, there is no such thing as 100% safe. I should have said “99.9% safe”.

I don’t agree with your idea that safe deposit boxes or vaults in peoples’ homes are a good way of seeking safety. Neither of those are desperately safe in that they tend to get burgled (though of course you can cover that with insurance).

Plus as far as storing central bank issued money goes, physically transferring wads of £20 notes into safe deposit boxes is a very crude and expensive way of storing money, given that the same thing can be done electronically.

Re your last paragraph (inflation etc), those of us concerned with bank reform are concerned with safety in the sense of avoiding “losing everything” as happened to some depositors in Cyprus. Of course holding money is not safe in that inflation eats away at it. But no one with significant net assets holds the bulk of their assets in the form of money. Most people’s wealth is in the form of houses, which in the long term is a good hedge against inflation.

Ralph:

note the choice is still available in my article. You either deposit your money in the bank and the bank warehouses it, or you lend your money in which case the bank invests it (for you). I’m pretty sure you’re arguing for the same thing my article discusses.

David, Glad we’re agreed on that. But it wasn’t very obvious to me from your article that you intended giving depositors the 99.9% safe option. Can I suggest you make that a bit clearer in future articles?

Fractional reserve banking would not last long in a free market. As Rothbard said, absent the govt underwriting the banks either directly through deposit insurance or indirectly through the central bank, you would not find a private insurance willing to cover a depositor’s funds in a FRB in a free market. Because fractional reserve banks always go bust after a credit boom caused by over-lending on fractions of reserves. So, FRB banking , if left to face the free market, would die out. No regulation required. Depositors , maybe after being burned once or twice in a bust , would vote with their feet.