[Editor’s note: this piece was first published at Zero Hedge, which has had several excellent articles tracking the effusions of the PBOC and their effect on credit markets]

Shortly after we exposed the real liquidity crisis facing Chinese banks recently (when no repo occurred and money market rates surged), China (very quietly) announced CNY 1 trillion of ‘Pledged Supplementary Lending’ (PSL) by the PBOC to China Development Bank. This first use of the facility “smacks of quantitative easing” according to StanChart’s Stephen Green, noting it is “deliberate and significant expansion of the PBOC’s balance sheet via creating bank reserves/cash” and likens the exercise to the UK’s Funding For Lending scheme. BofA is less convinced of the PBOC’s quantitative loosening, suggesting it is more like a targeted line of credit (focused on lowering the costs of funding) and arguing with a record “asset” creation by Chinese banks in Q1 does China really need standalone QE?

China still has a liquidity crisis without the help of the PBOC… (when last week the PBOC did not inject liquidty via repo, money market rates spiked to six-month highs…)

And so the PBOC decided to unleash PSL (via BofA)

The China Business News (CBN, 18 June), suggests that the PBoC has been preparing a new monetary policy tool named “Pledged Supplementary Lending” (PSL) as a new facility to provide base money and to guide medium-term interest rates. Within the big picture of interest rate liberalization, the central banks may wish to have a series of policy instruments at hand, guaranteeing the smooth transition of the monetary policy making framework from quantity tools towards price tools.

PSL: a new tool for base money creation

Since end-1990s, China’s major source of base money expansion was through PBoC’s purchase of FX exchanges, but money created from FX inflows outpaced money demand of the economy. To sterilize excess inflows, the PBoC imposed quite high required reserve ratio (RRR) for banks at 17.5-20.0% currently, and issued its own bills to banks to lock up cash. With FX inflows most likely to slow after CNY/USD stopped its one-way appreciation and China’s current account surplus narrowed, there could be less need for sterilization. The PBoC may instead need to expand its monetary base with sources other than FX inflows, and PSL could become an important tool in this regard.

…and a tool for impacting medium-term policy rate

Moreover, we interpret the introduction of the PSL as echoing the remarks by PBoC Governor Zhou Xiaochuan in a Finance Forum this May that “the policy tool could be a short-term policy rate or a range of it, possibly plus a medium-term interest rate”. The PBoC is likely to gradually set short-term interbank rates as new benchmark rates while using a new policy scheme similar to the rate corridor operating frameworks currently used in dozens of other economies. A medium-term policy rate could be desirable for helping the transmission of short-term policy rate to longer tenors so that the PBoC could manage financing costs for the real economy.

Key features of PSL

Through PSL, the PBoC could provide liquidity with maturity of 3-month to a few years to commercial banks for credit expansion. In some way, it could be similar to relending, and it’s reported that the PBoC has recently provided relending to several policy and commercial banks to support credit to certain areas, such as public infrastructure, social housing, rural sector and smaller enterprises.

However, PSL could be designed more sophisticatedly and serve a much bigger monetary role compared to relending.

First, no collateral is required for relending so there is credit risk associated with it. By contrast, PSL most likely will require certain types of eligible collaterals from banks.

Second, the information disclosure for relending is quite discretionary, and the market may not know the timing, amount and interest rates of relending. If the PBoC wishes to use PSL to guide medium-term market rate, the PBoC perhaps need to set up proper mechanism to disclose PSL operations.

Third, relending nowadays is mostly used by the PBoC to support specific sectors or used as emergency funding facility to certain banks. PSL could be a standing liquidity facility, at least for a considerable period of time during China’s interest rate liberalization.

Some think China’s PSL Is QE (via Market News International reports),

Standard Chartered economist Stephen Green says in a note that reports of the CNY1 trillion in Pledged Supplementary Lending (PSL) that the People’s Bank of China recently conducted in the market smacks of quantitative easing. He notes that the funds which have been relent to China Development Bank are “deliberate and significant expansion of the PBOC’s balance sheet via creating bank reserves/cash” and likens the exercise to the UK’s Funding For Lending scheme. CDB’s balance sheet reflects the transfer of funds, even if the PBOC’s doesn’t.

The CNY1 trillion reported — no details confirmed by the PBOC yet — will wind up in the broader economy and boost demand and “sends a signal that the PBOC is in the mood for quantitative loosening,” Green writes

The impact will depend on whether the details are correct and if all the funds have been transferred already, or if it’s just a jumped up credit facility that CDB will be allowed to tap in stages.

But BofA believes it is more likely a targeted rate cut tool (via BofA)

The investment community and media are assessing the possible form and consequence of the first case of Pledged Supplementary Lending (PSL) by PBoC to China Development Bank (CDB). The planned total amount of RMB1.0tn of PSL is more like a line of credit rather than a direct Quantitative Easing (QE). The new facility can be understood as a “targeted rate cut” rather than QE. We reckon that only some amount has been withdrawn by CDB so far. Despite its initial focus on shantytown redevelopment, we believe the lending could boost the overall liquidity and offer extra help to interbank market. Depending on its timespan of depletion, the actual impact on growth could be limited but sufficient to help deliver the growth target.

Relending/PSL to CDB yet to be confirmed

The reported debut of PSL was not a straightforward one. The initial news report by China Business News gave no clues on many of the details of the deal expect for the total amount and purpose of the lending. With the limited information, we believe the lending arrangement is most likely a credit line offered by PBoC to CDB. The total amount of RMB1.0tn was not likely being used already even for a strong June money and credit data. According to PBoC balance sheet, its claims to other financial institutions increased by RMB150bn in April and May. If the full amount has been withdrawn by CDB, it is equivalent to say PBoC conducted RMB850bn net injection via CDB in June, since CDB has to park the massive deposits in commercial banks. We assess the amount could be too big for the market as the interbank rates were still rising to the mid-year regulatory assessment. The PBoC could disclose the June balance after first week of August, we expect some increase of PBoC’s claims on banks, but would be much less than RMB850bn.

Difference with expected one

In our introductory PSL report, we argue that the operation has its root in policy reform of major central banks. However, we do not wish to compare literally with these existing instruments, namely ECB’s TLTRO or BoE’s FLS. Admittedly, the PBoC has its discretion to design the tailor-made currency arrangement due to the special nature of policy need. However, the opaque operation of PSL will eventually prove it a temporary arrangement and perhaps not serving as an example for other PSLs for its initial policy design to be achieved. According to Governor Zhou, the PSL is supposed to provide a reference to medium-term interest rate, which is missing in today’s case.

The focus is lowering cost of funding

We have been arguing that relending is a Chinese version of QE. Although relending is granted to certain banks, but there is no restriction on how banks use the funding. However, we believe PSL is more than that. The purpose of CDB’s PSL has been narrowed down to shantytown redevelopment, an area usually demands fiscal budget or subsidy in the past. Funding cost is the key to this arrangement.

Indeed, the PBoC has been working hard to reduce the cost of funding in the economy since massive easing is not an option under the increasing leverage of the economy. A currency-depreciation easing has been initiated by PBoC to bring down the interbank rate. Since then the central bank carefully manages the OMO in order to prevent liquidity squeeze from happening. On 24 July, State Council and CBRC have introduced workable measures to reduce funding cost of small and micro-enterprises.

Impact of the lending

PSL is not a direct QE, but there could be some side effect by this targeted lending. PSL to CDB means the funding demand and provision come hand-inhand. Targeted credit easing by nature is a requirement by targeted areas demanding policy support, which could be SMEs, infrastructure or social housing. In this regard, it is not surprising to see more PSL to support infrastructure financing. In addition to the direct impact on those targeted areas, we expect the overall funding cost could benefit from liquidity spillover.

Market reaction

Since the news about PSL with CDB last Monday, we have seen a rally in the Shanghai Composite Index. However we believe multiple factors may have contributed to the rebound in the stock market including: (1) better than expected macro data in 2Q/June and HSBC PMI surprising on the upside leading to improved sentiment; (2) The State Council and the CBRC have introduced measures to reduce funding cost of small and micro-enterprises; (3) More property easing with the removal of home purchase restrictions in several cities. PSL could have contributed to the improved sentiment on expectation of further easing.

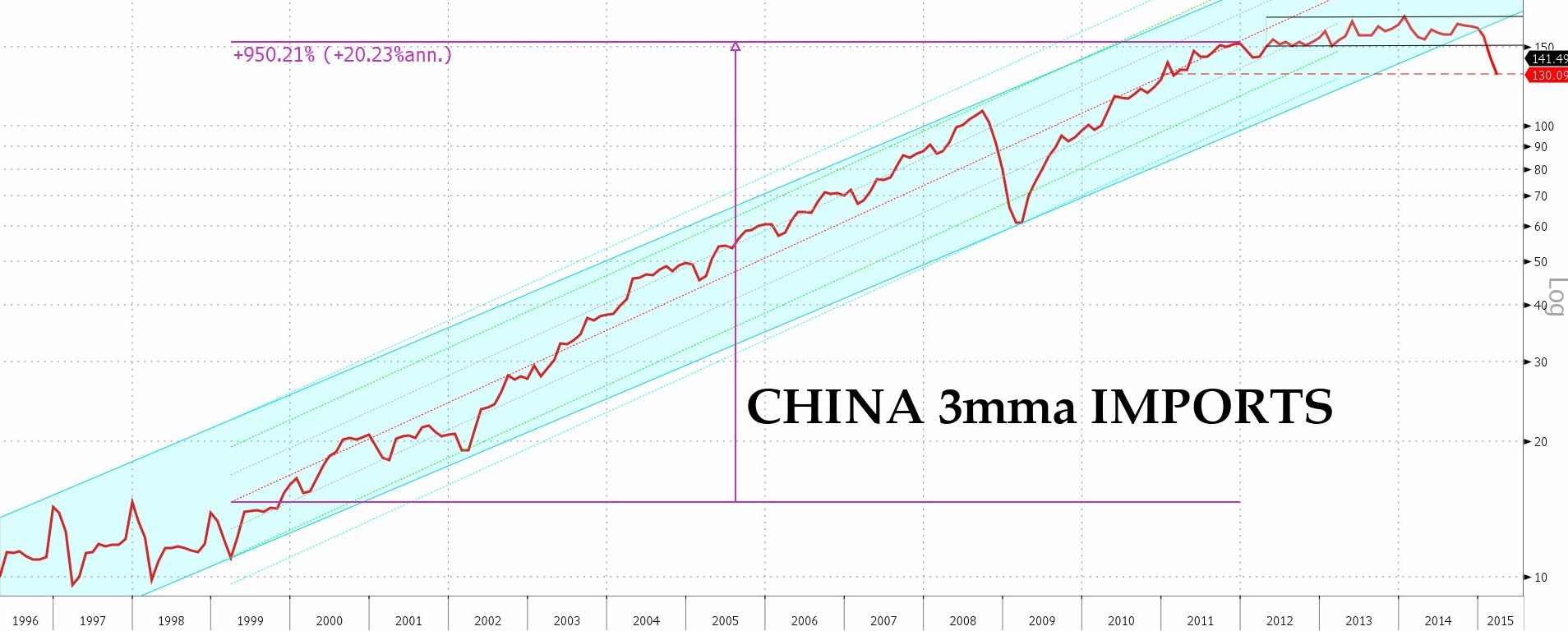

Since as we noted previously, China’s massive bank asset creation (dwarfing the US) hardly looks like it needs QE…

As Bank Assets exploded in Q1…

dramatically outpacing the US…

Unless something really bad is going on that needs an even bigger bucket of liquidity.

* * *

So whatever way you look at it, the PBOC thinks China needs more credit (through one channel or another) to keep the ponzi alive. Anyone still harboring any belief in reform, rotation to consumerism is sadly mistaken. One day of illiquidity appears to have been enough to prove that they need to keep the pipes wide open. The question is where that hot money flows as they clamp down (or not) on external funding channels.

Notably CNY has strengthened recently as the PSL appears to have encouraged flows back into China.

* * *

The plot thickened a little this evening as China news reports:

- *CBRC ALLOWS CHINA DEV. BANK TO START HOUSING FINANCE BUSINESS

- *CHINA APPROVES CDB’S HOME FINANCE DEPT TO START BUSINESS: NEWS

Thus it appears the PSL is a QE/funding channel directly aimed at supporting housing. CNY 1 trillion to start and maybe China is trying to create a “Fannie-Mae” for China.