There are two kinds of credit: that which would be offered in a market economy with sound money and banking (true credit), and that which is made possible only through a system of central banking, artificially low interest rates, and fractional reserves (false credit).

Banks cannot expand true credit as such. All that they can do in reality is to facilitate the transfer of a given pool of savings from savers (i.e., those lending to the bank) to borrowers.

Consider the case of a baker who bakes ten loaves of bread. Out of his stock of real wealth (ten loaves of bread), the baker consumes two loaves and saves eight.

He lends his eight remaining loaves to the shoemaker in return for a pair of shoes in one-week’s time.

Note that credit here is the transfer of ”real stuff,” i.e., eight saved loaves of bread from the baker to the shoemaker in exchange for a future pair of shoes.

Also, observe that the amount of real savings determines the amount of available credit. If the baker had saved only four loaves of bread, the amount of credit would have only been four loaves instead of eight.

Note that the saved loaves of bread provide support to the shoemaker. That is, the bread sustains the shoemaker while he is busy making shoes.

This means that credit, by sustaining the shoemaker, gives rise to the production of shoes and therefore to the formation of more real wealth. This is the path to real economic growth.

Money and Credit

The introduction of money does not alter the essence of what credit is. Instead of lending his eight loaves of bread to the shoemaker, the baker can now exchange his saved eight loaves of bread for eight dollars and then lend them to the shoemaker.

With eight dollars the shoemaker can secure either eight loaves of bread or other goods to support him while he is engaged in the making of shoes. The baker is supplying the shoemaker with the facility to access the pool of real savings, which among other things also has eight loaves of bread that the baker has produced. Also note that without real savings the lending of money is an exercise in futility.

Money fulfills the role of a medium of exchange. Thus, when the baker exchanges his eight loaves for eight dollars he retains his real savings, so to speak, by means of the eight dollars.

The money in his possession will enable him, when he deems it necessary, to reclaim his eight loaves of bread or to secure any other goods and services.

There is one provision here that the flow of production of goods continues. Without the existence of goods, the money in the baker’s possession will be useless.

The existence of banks does not alter the essence of credit. Instead of the baker lending his money directly to the shoemaker, the baker lends his money to the bank, which in turn lends it to the shoemaker. In the process the baker earns interest for his loan, while the bank earns a commission for facilitating the transfer of money between the baker and the shoemaker.

The benefit that the shoemaker receives is that he can now secure real resources in order to be able to engage in his making of shoes.

Despite the apparent complexity that the banking system introduces, the essence of credit remains the transfer of saved real stuff from lender to borrower.

Without an increase in the pool of real savings, banks cannot create more credit. At the heart of the expansion of good credit by the banking system is an expansion of real savings.

Now, when the baker lends his eight dollars we must remember that he has exchanged for these dollars eight saved loaves of bread. In other words, he has exchanged something for eight dollars. So when a bank lends those eight dollars to the shoemaker, the bank lends fully “backed” dollars, so to speak.

False Credit: An Agent of Economic Destruction

Trouble emerges when instead of lending fully backed money, a bank engages in issuing empty money (fractional reserve banking) that is backed by nothing.

When unbacked money is created, it masquerades as genuine money that is supposedly supported by real stuff. In reality however, nothing has been saved. So when such money is issued, it cannot help the shoemaker since the pieces of empty paper cannot support him in producing shoes — what he needs instead is bread.

Since the printed money masquerades as proper money it can be used to divert bread from some other activities and thereby weaken those activities. This is what the diversion of real wealth by means of money out of “thin air” is all about.

If the extra eight loaves of bread weren’t produced and saved, it is not possible to have more shoes without hurting some other activities, which are much higher on the priority list of consumers as far as life and well-being is concerned. This in turn also means that unbacked credit cannot be an agent of economic growth.

Rather than facilitating the transfer of savings across the economy to wealth generating activities, when banks issue unbacked credit they are in fact setting in motion a weakening of the process of wealth formation.

It has to be realized that banks cannot pursue unbacked lending on an ongoing basis without the existence of the central bank. The central bank, by means of monetary pumping, makes sure that the expansion of unbacked credit doesn’t cause banks to bankrupt each other.

We can thus conclude that as long as the increase in lending is fully backed by real savings it must be regarded as good news since it promotes the formation of real wealth. False credit, which is generated out of “thin air,” is bad news since credit which is unbacked by real savings is an agent of economic destruction.

This has a persuasive ring to it.

I am not clear about how the reallity can be created.

In this model someone has to save before somone can lend.

What happens when the population increases and the total amount of money is the same?

Also the value of money is not constant whatever we may try to do to fix it. Therefore the total quantity of money has to be varied.

At some point some money has to be created and shared with EVERYONE, not some people.

The situation as it is at present is something that I have not been able to determine.

It is said that 97.5% of money (not sure which currency) is created by the banks – money out of thin air.

Somehow that becomes someone else’s savings and another person’s spending money.

I am not at all clear how much of those savings are backed by anything or even whether the need to be backed by anything.

What I have suggested is that as that lent money gets repaid an equivalent amount of money-for-lending should be created so that we do not reduce the stock of money (cash and deposits) as we change over from fractional banking to an economy that has control over the total demand in the economy – or better cotrol anyway.

Where will we end up in that case?

How much of the money in the banks and in cash will then be saved money and how much will be deposits / credit made available by the Money Supply Authority, bid for at interest by lenders and borrowers?

Can anyone answer that question?

Another point of interest is this:

How would those figures differ if the fractional banking system had never been created and we had used this system from outset?

I suspect that the proportion of total economic activity in the borrowing dependent sectors would be different anyway.

Any comments?

Edward,

You need to introduce prices in your analysis. Any quantity of money would do to satisfy its demand; what would change would be its purchasing power. A growing population and a growing economy would mean falling prices under sound money and true credit. In fact that is what happened during the last quarter of the XIX Century. This can be considered the golden era of capitalism which was sadly interrupted by progressivism and the wars.

Edward,

In addition to the point above about introducing prices into your analysis, another problem is in definitions, esp money v credit. If you correct your inquiry for these errors, your thinking will tighten up.

Money is strictly medium of exchange. It is used to extinguish debt. Credit is and agreement to pay later, not the same thing. Currency can be either a warehouse receipt for gold (medium of exchange) or credit (fiat currency). Gets confusing fast, doesn’t it? That is on purpose.

When I was a kid, the grocer and pharmacist gave my parents till the end of the month to pay. The wholesalers gave the retailers thirty days to pay. manufacturers gave wholesalers 30 days, materials suppliers gave mfgr 30 days, extraction gave material makers 30 days… most of the economy was on credit, all asset backed (Shostak’s good credit) and none of it at interest.

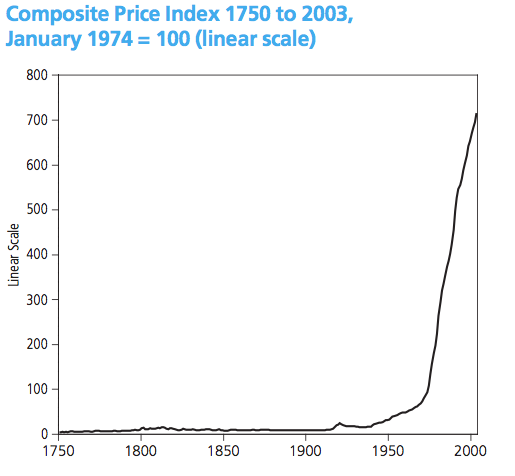

Then came 1971, Nixon went off the gold standard lite, and banks experimented with lending the bad credit Shostak mentions: asset less backed credit.

Notice what a Moslem correspondent pointed out: in the massive private credit outlined above, nonpayment meant the lender took a loss, and the borrower lost nor gained nothing. When credit is loaned with no asset behind it, and the borrower fails to pay back, the bank loses nothing (for it lent nothing) but the borrower loses some other secured asset (home?). The former is managed at a human scale by 350 million (in the usa) people, the latter is managed by six banks. In the former credit expands with population as human interaction recommends its asset-backed introduction. The six banks are agents of social engineering on an industrial scale.

To the extent we have false credit (92%?) minus what false credit accidently is invested in true economy pursuits, is the degree to which this economy will fail, plus, what with regression to the mean. Imponderable. But will there be enough people who recall that pitch perfect, human scale, unitive and creative credit system to revive it after the crack-up bust?

John Spiers